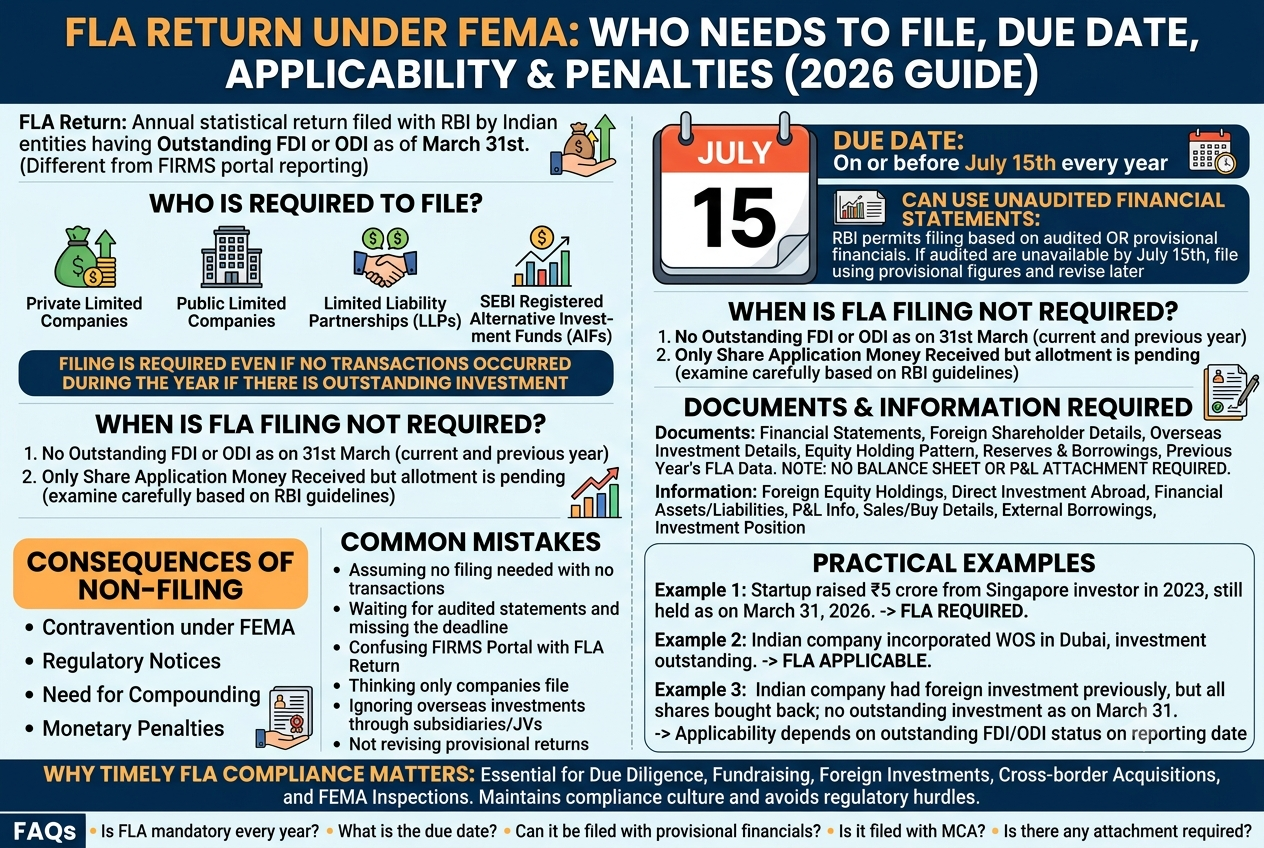

If your company has received Foreign Direct Investment (FDI) or has made Overseas Direct Investment (ODI), filing the Foreign Liabilities and Assets (FLA) Return is an annual FEMA compliance that cannot be overlooked.

Every year, many startups, private limited companies, LLPs, and Indian subsidiaries of foreign companies assume that since there were no transactions during the year, no filing is required. Unfortunately, that assumption can lead to FEMA non-compliance.

Need Help with FLA Return Filing Under FEMA?

The Foreign Liabilities and Assets (FLA) Return is an annual return required to be filed with the Reserve Bank of India (RBI) by Indian entities having:

as on 31st March of the relevant financial year.

The purpose of the return is to help RBI compile India’s external sector statistics and check foreign investments.

It is important to note that the FLA Return is a statistical return and is different from reporting made through the FIRMS Portal (such as FC-GPR, FC-TRS, LLP(I), etc.).

The following Indian resident entities are generally required to file the FLA Return if they have outstanding FDI or ODI as on 31st March:

Many businesses unnecessarily worry about FLA filing even when it may not apply.

Generally, filing is not required where:

If there is no outstanding foreign investment or overseas investment as on 31st March of both the current and previous financial year.

Where only share application money was received but no outstanding FDI exists as on 31st March, filing may not be required.

However, every case should be examined carefully based on RBI guidelines.

The FLA Return must be filed on or before 15th July every year.

The reporting is based on the financial position as on 31st March immediately preceding the filing.

Yes.

One of the biggest misconceptions is that businesses must wait for statutory audit completion.

The RBI permits filing based on:

If audited accounts are not available before 15th July, the entity should:

Unlike many ROC filings, the FLA Return is relatively document-light.

Typically, businesses need:

Importantly,

No Balance Sheet or Profit & Loss Account is required to be attached while filing the FLA Return.

The return captures information relating to:

The reporting should reconcile with the entity’s financial statements.

Many businesses treat the FLA Return as a routine compliance until they face regulatory scrutiny.

Failure to file the return within the prescribed timeline is treated as a contravention under the Foreign Exchange Management Act (FEMA).

Depending upon the facts of the case, this may result in:

Over the years, we’ve observed several recurring mistakes:

❌ Assuming no filing is required because there were no transactions during the year

❌ Waiting for audited financial statements and missing the deadline

❌ Confusing FIRMS Portal reporting with FLA Return

❌ Believing only companies are required to file

❌ Ignoring overseas investments made through subsidiaries or joint ventures

❌ Not revising provisional returns after audit

Example 1

A startup raised ₹5 crore from a Singapore investor in 2023.

The investor continues to hold shares as on 31st March 2026.

FLA Return is required.

Example 2

An Indian company incorporated a wholly owned subsidiary in Dubai.

The investment remains outstanding.

FLA Return is applicable.

Example 3

An Indian company had foreign investment earlier, but all shares were bought back and no outstanding foreign investment exists as on 31st March.

The applicability would depend upon whether any outstanding FDI/ODI remains on the reporting date.

Many businesses focus only on Companies Act compliances and income tax filings while overlooking FEMA reporting.

However, during:

FLA compliance is often one of the first items reviewed.

Maintaining timely filings reflects a strong compliance culture and avoids unnecessary regulatory hurdles.

The FLA Return may be a single annual filing, but its significance under FEMA should not be underestimated. Even if there are no fresh foreign investment transactions during the year, the existence of outstanding FDI or ODI as on 31st March may trigger the filing rule.

Since the return can be filed using provisional financial statements and revised later, businesses should avoid delaying the filing until the audit is complete.

If your business has foreign shareholders, overseas subsidiaries, or any form of cross-border investment, it is advisable to review the applicability of the FLA Return well before 15th July each year.