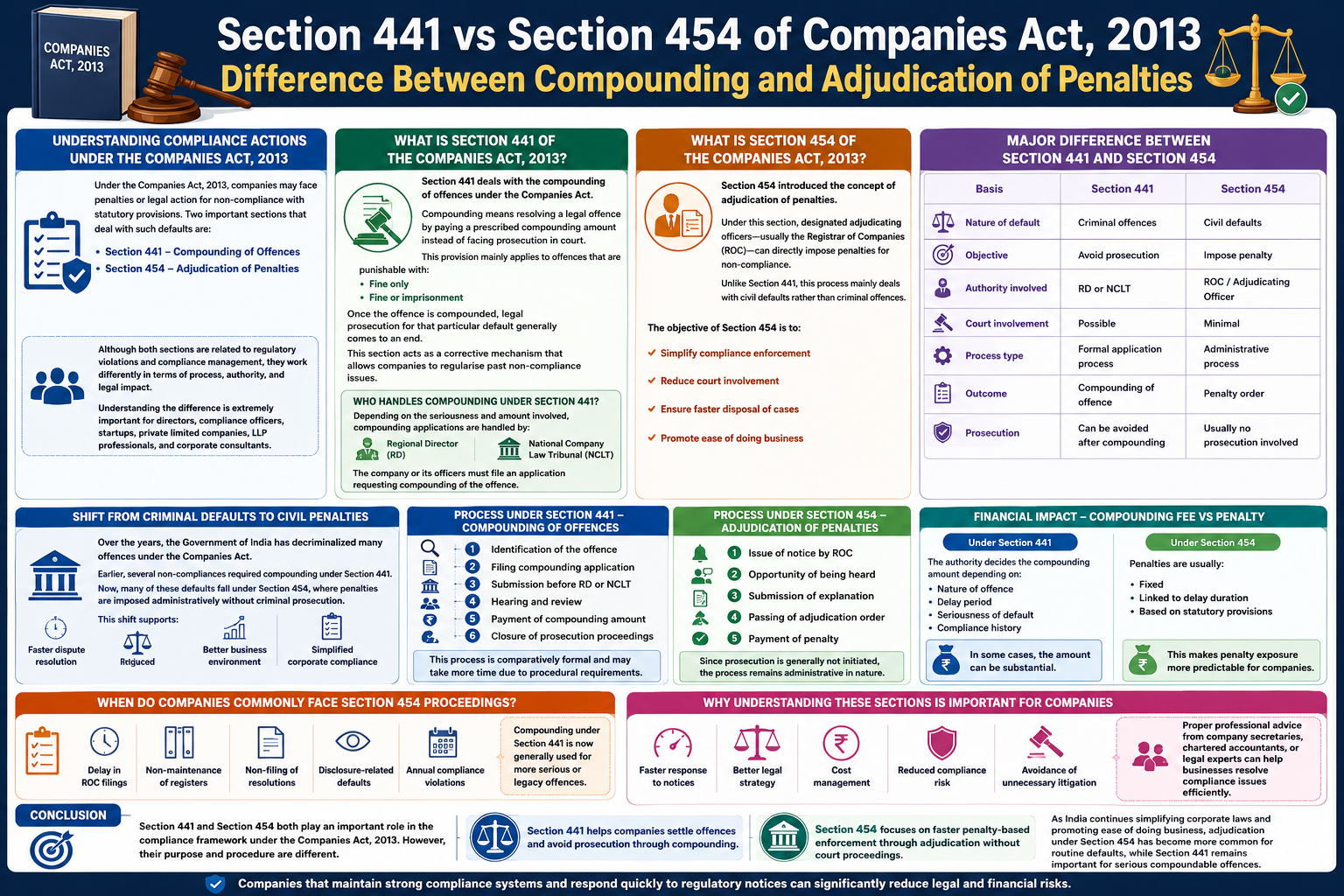

Under the Companies Act, 2013, companies may face penalties or legal action for non-compliance with statutory provisions. Two important sections that deal with such defaults are the following:

Although both sections are related to regulatory violations and compliance management, they work differently in terms of process, authority, and legal impact.

For company directors, compliance officers, startups, private limited companies, LLP professionals, and corporate consultants, understanding the difference between these two provisions is extremely important.

Section 441 deals with the compounding of offenses under the Companies Act.

Compounding means resolving a legal offense by paying a prescribed compounding amount instead of facing prosecution in court.

This provision mainly applies to offenses that are punishable with:

Once the offense is compounded, legal prosecution for that particular default generally comes to an end.

This section acts as a corrective mechanism that allows companies to regularize past non-compliance issues.

Depending on the seriousness and amount involved, compounding applications are handled by:

The company or its officers must file an application requesting compounding of the offense.

Section 454 introduced the concept of adjudication of penalties.

Under this section, designated adjudicating officers—usually the Registrar of Companies (ROC)—can directly impose penalties for non-compliance.

Unlike Section 441, this process mainly deals with civil defaults rather than criminal offenses.

The objective of Section 454 is to:

The biggest difference lies in the nature of the default.

Basis | Section 441 | Section 454 |

Nature of default | Criminal offences | Civil defaults |

Objective | Avoid prosecution | Impose a penalty. |

Authority involved | RD or NCLT | ROC / Adjudicating Officer |

Court involvement | Possible | Minimal |

Process type | Formal application process | Administrative process |

Outcome | Compounding of offence | Penalty order |

Prosecution | Can be avoided after compounding | Usually no prosecution involved |

Over the years, the Government of India has decriminalized many offenses under the Companies Act.

Earlier, several non-compliances required compounding under Section 441.

Now, many of these defaults fall under Section 454, where penalties are imposed administratively without criminal prosecution.

This shift supports:

The compounding process usually involves:

This process is comparatively formal and may take more time due to procedural requirements.

The adjudication mechanism under Section 454 is faster and simpler.

Typical processes include the following:

Since prosecution is generally not initiated, the process remains administrative in nature.

Under Section 441, the authority decides the compounding amount depending on the following:

In some cases, the amount can be substantial.

Under Section 454, penalties are usually

This makes penalty exposure more predictable for companies.

Today, most routine compliance defaults are handled under Section 454, including the following:

Compounding under Section 441 is now generally used for more serious or legacy offenses.

Businesses should clearly understand whether a default falls under the following:

This helps in:

Proper professional advice from company secretaries, chartered accountants, or legal experts can help businesses resolve compliance issues efficiently.

H2: Conclusion

Section 441 and Section 454 both play an important role in the compliance framework under the Companies Act, 2013.

However, their purpose and procedure are different.

As India continues simplifying corporate laws and promoting ease of doing business, adjudication under Section 454 has become more common for routine defaults, while Section 441 remains important for serious compoundable offenses.

Companies that maintain strong compliance systems and respond quickly to regulatory notices can significantly reduce legal and financial risks.