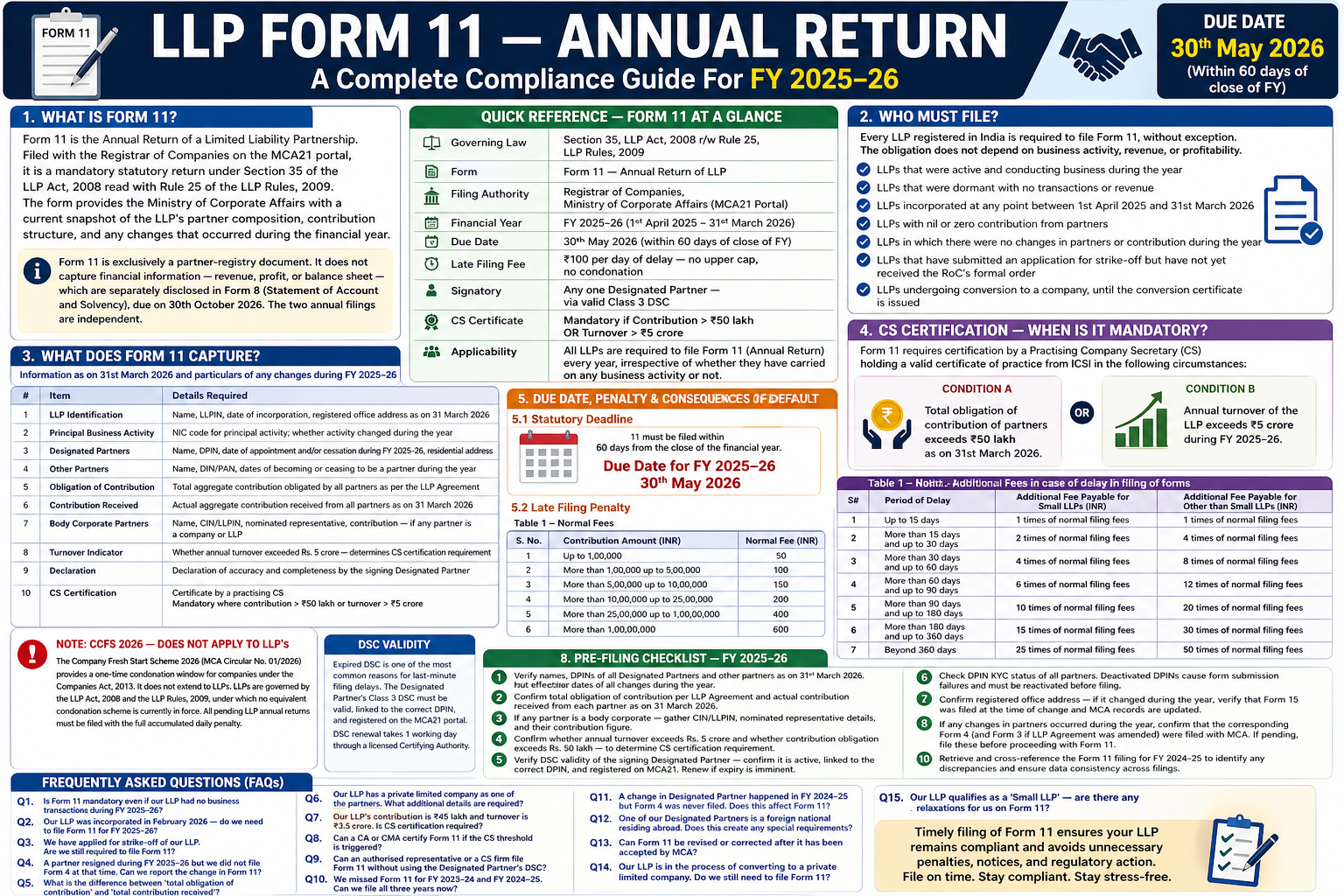

Form 11 is the Annual Return of a Limited Liability Partnership. Filed with the Registrar of Companies on the MCA21 portal, it is a mandatory statutory return under Section 35 of the LLP Act, 2008 read with Rule 25 of the LLP Rules, 2009. The form provides the Ministry of Corporate Affairs with a current snapshot of the LLP’s partner composition, contribution structure, and any changes that occurred during the financial year.

Form 11 is exclusively a partner-registry document. It does not capture financial information — revenue, profit, or balance sheet — which are separately disclosed in Form 8 (Statement of Account and Solvency), due on 30th October 2026. The two annual filings are independent.

QUICK REFERENCE — FORM 11 AT A GLANCE | |

Governing Law | Section 35, LLP Act, 2008 r/w Rule 25, LLP Rules, 2009 |

Form | Form 11 — Annual Return of LLP |

Filing Authority | Registrar of Companies, Ministry of Corporate Affairs (MCA21 Portal) |

Financial Year | FY 2025–26 (1st April 2025 – 31st March 2026) |

Due Date | 30th May 2026 (within 60 days of close of FY) |

Late Filing Fee | ₹100 per day of delay — no upper cap, no condonation |

Signatory | Any one Designated Partner — via valid Class 3 DSC |

CS Certificate | Mandatory if Contribution > ₹50 lakh OR Turnover > ₹5 crore |

Applicability | All LLPs are required to file Form 11 (Annual Return) every year, irrespective of whether they have carried on any business activity or not. |

Every LLP registered in India is required to file Form 11, without exception. The obligation does not depend on business activity, revenue, or profitability.

The following categories of LLPs must file Form 11 for FY 2025–26:

Form 11 requires the following information reflecting the position of the LLP as on 31st March 2026, along with particulars of any changes during FY 2025–26:

# | Item | Details Required |

1 | LLP Identification | Name, LLPIN, date of incorporation, registered office address as on 31 March 2026 |

2 | Principal Business Activity | NIC code for principal activity; whether activity changed during the year |

3 | Designated Partners | Name, DPIN, date of appointment and/or cessation during FY 2025-26, residential address |

4 | Other Partners | Name, DIN/PAN, dates of becoming or ceasing to be a partner during the year |

5 | Obligation of Contribution | Total aggregate contribution obligated by all partners as per the LLP Agreement |

6 | Contribution Received | Actual aggregate contribution received from all partners as on 31 March 2026 |

7 | Body Corporate Partners | Name, CIN/LLPIN, nominated representative, contribution — if any partner is a company or LLP |

8 | Turnover Indicator | Whether annual turnover exceeded Rs. 5 crore — determines CS certification requirement |

9 | Declaration | Declaration of accuracy and completeness by the signing Designated Partner |

10 | CS Certification | Certificate by a practising CS Mandatory where contribution > Rs. 50 lakh or turnover > Rs. 5 crore |

Form 11 requires certification by a Practising Company Secretary (CS) holding a valid certificate of practice from ICSI in the following circumstances:

OR

The Statutory Deadline: Form 11 must be filed within 60 days from the close of the financial year. For FY 2025–26 (ended 31st March 2026), the filing due date is 30th May 2026.

Table 1-Normal fees

S. No. | Contribution Amount (INR) | Normal Fee (INR) |

1 | Up to 1,00,000 | 50 |

2 | More than 1,00,000 up to 5,00,000 | 100 |

3 | More than 5,00,000 up to 10,00,000 | 150 |

4 | More than 10,00,000 up to 25,00,000 | 200 |

5 | More than 25,00,000 up to 1,00,00,000 | 400 |

6 | More than 1,00,00,000 | 600 |

Table 2- Additional Fees in case of delay in filing of forms

S# | Period of delay | Additional fee payable for Small LLPs (INR) | Additional fee payable for Other than Small LLPs (INR) |

1 | Up to 15 days | 1 times of normal filing fees | 1 times of normal filing fees |

2 | More than 15 days and up to 30 days | 2 times of normal filing fees | 4 times of normal filing fees |

3 | More than 30 days and up to 60 days | 4 times of normal filing fees | 8 times of normal filing fees |

4 | More than 60 days and up to 90 days | 6 times of normal filing fees | 12 times of normal filing fees |

5 | More than 90 days and up to 180 days | 10 times of normal filing fees | 20 times of normal filing fees |

6 | More than 180 days and up to 360 days | 15 times of normal filing fees | 30 times of normal filing fees |

7. | Beyond 360 days | 25 times of normal filing fees | 50 times of normal filing fees |

NOTE:

CCFS 2026 — Does Not Apply to LLP’S

The Company Fresh Start Scheme 2026 (MCA Circular No. 01/2026) provides a one-time condonation window for companies under the Companies Act, 2013. It does not extend to LLPs. LLPs are governed by the LLP Act, 2008 and the LLP Rules, 2009, under which no equivalent condonation scheme is currently in force. All pending LLP annual returns must be filed with the full accumulated daily penalty.

DSC VALIDITY

Expired DSC is one of the most common reasons for last-minute filing delays. The Designated Partner’s Class 3 DSC must be valid, linked to the correct DPIN, and registered on the MCA21 portal. DSC renewal takes 1 working days through a licensed Certifying Authority.

The following checklist covers all actions required before Form 11 can be filed without complications:

# | Action Item |

1 | Verify names, DPINs of all Designated Partners and other partners as on 31st March 2026. Note effective dates of all changes during the year. |

2 | Confirm total obligation of contribution per LLP Agreement and actual contribution received from each partner as on 31 March 2026. |

3 | If any partner is a body corporate — gather CIN/LLPIN, nominated representative details, and their contribution figure. |

4 | Confirm whether annual turnover exceeds Rs. 5 crore and whether contribution obligation exceeds Rs. 50 lakh — to determine CS certification requirement. |

6 | Verify DSC validity of the signing Designated Partner — confirm it is active, linked to the correct DPIN, and registered on MCA21. Renew if expiry is imminent. |

7 | Check DPIN KYC status of all partners. Deactivated DPINs cause form submission failures and must be reactivated before filing. |

8 | Confirm registered office address — if it changed during the year, verify that Form 15 was filed at the time of change and MCA records are updated. |

9 | If any changes in partners occurred during the year, confirm that the corresponding Form 4 (and Form 3 if LLP Agreement was amended) were filed with MCA. If pending, file these before proceeding with Form 11. |

10 | Retrieve and cross-reference the Form 11 filing for FY 2024-25 to identify any discrepancies and ensure data consistency across filings. |