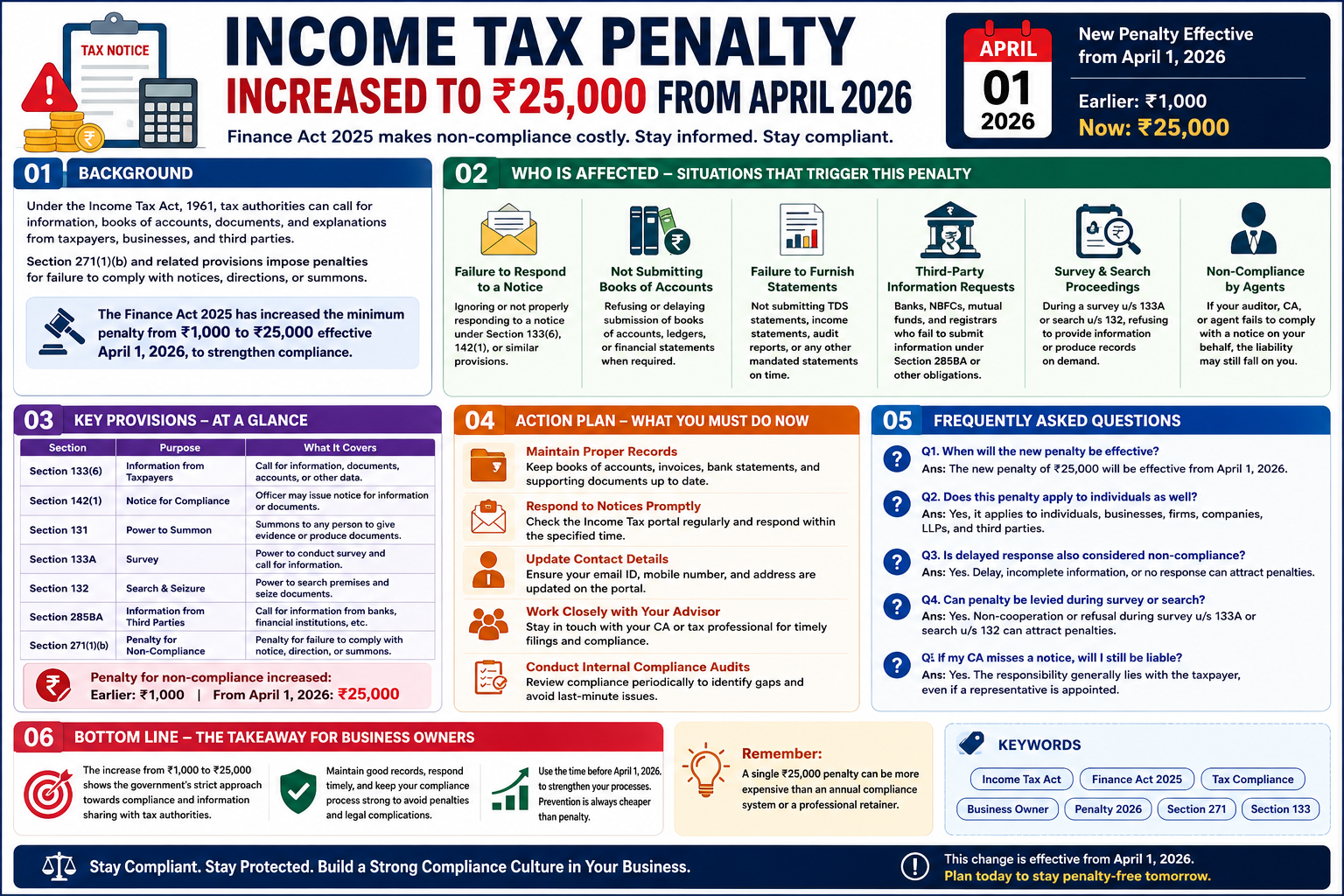

The Government of India has significantly increased penalties for non-compliance under the Income Tax Act, 1961.

Through the Finance Act 2025, the earlier penalty of ₹1,000 for failing to respond to tax notices or furnish required information has now been increased to ₹25,000.

This change takes effect on April 1, 2026.

The move is aimed at strengthening tax compliance and ensuring businesses, professionals, and financial institutions respond promptly to notices issued by the Income Tax Department.

For many businesses that previously ignored tax notices due to low penalties, the compliance risk is now much higher.

Under the Income Tax Act, tax authorities have the legal power to request:

These powers are exercised through sections such as the following:

If a taxpayer, business, or third party fails to comply with these notices or directions, penalties may be imposed.

Earlier, many taxpayers treated the ₹1,000 penalty as a minor issue.

However, from April 2026, the government has sharply increased the penalty amount to improve response rates and transparency.

Particulars | Earlier Penalty | New Penalty from April 2026 |

Failure to comply with notices or summons | ₹1,000 | ₹25,000 |

This revised penalty applies to multiple types of non-compliance situations.

Many business owners assume this penalty applies only during tax raids or investigations. In reality, the scope is much wider.

If you fail to reply to notices issued under sections like

The department may impose the revised penalty.

This includes delayed responses, incomplete submissions, or total non-response.

Businesses may be asked to provide:

Failure to submit these documents within the prescribed timeline may result in penalties.

Penalties may also apply for delays in submitting:

Timely filing has now become more critical than ever.

The penalty is not limited to taxpayers alone.

It may also apply to:

if they fail to furnish the required information under Section 285BA or related provisions.

During:

officials may ask for records or explanations.

Refusal, delay, or obstruction can attract heavy penalties.

Even if your chartered accountant or authorized representative handles compliance on your behalf, the responsibility may still remain with you as the taxpayer.

If your compliance team ignores the notices, the business owner may still face the penalty.

The government is moving toward stricter data monitoring and digital tax enforcement.

Income tax authorities now rely heavily on:

As a result, non-response or delayed submissions are more likely to be detected quickly.

The higher penalty is intended to force timely cooperation with tax authorities.

Businesses should start strengthening internal tax compliance systems immediately.

Ensure that all books of accounts and supporting documents are updated regularly.

Never ignore notices received through:

Even if additional time is needed, please file the proper replies.

Incorrect email IDs or mobile numbers may result in missed notices.

Update all details on the Income Tax portal regularly.

Businesses should maintain active communication with:

This reduces the risk of missed deadlines.

Periodic compliance audits can help identify:

before penalties arise.

The increase from ₹1,000 to ₹25,000 clearly shows that the government is taking tax compliance much more seriously.

Ignoring notices, delaying submissions, or maintaining poor records can now become expensive for businesses.

Companies that maintain proper documentation, respond on time, and work closely with professional advisors are unlikely to face difficulties.

Before April 2026, businesses should review their compliance systems and strengthen internal processes to avoid unnecessary penalties and regulatory scrutiny.