Every financial year, lakhs of startup founders and MSME owners across India face a critical question: Should I opt for the New Tax Regime or stick with the Old Tax Regime? With the Union Budget 2025 bringing significant tweaks to both systems, this decision carries more weight than ever. Making the wrong choice could cost your business anywhere from INR 50,000 to several lakhs in avoidable tax outgo.

In this detailed guide, we break down both regimes, compare them head-to-head with real Indian business scenarios, and give you a clear framework to choose the one that maximises your take-home income.

India’s personal income tax system currently offers two parallel structures for individuals and sole proprietors filing under individual capacity. Companies and LLPs have separate tax rates, but for startup founders drawing salary or income as proprietors, this choice matters enormously.

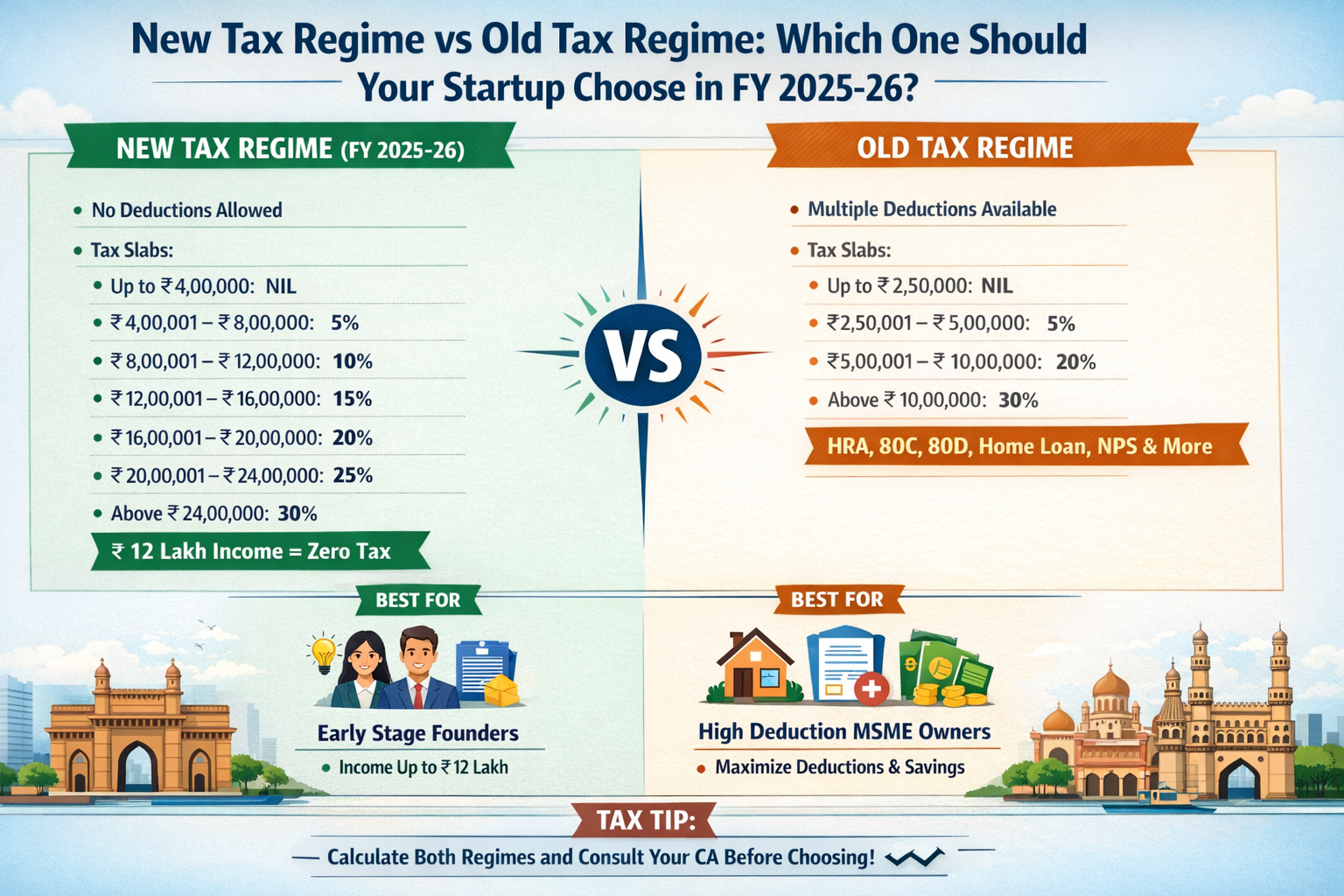

The Old Regime has been around for decades. It allows taxpayers to claim a wide array of deductions and exemptions including House Rent Allowance (HRA), Leave Travel Allowance (LTA), Section 80C investments up to INR 1,50,000, Section 80D health insurance premiums up to INR 25,000, home loan interest deductions, National Pension System (NPS) contributions under Section 80CCD, and standard deduction of INR 50,000 for salaried individuals.

The New Tax Regime offers reduced tax rates but eliminates most deductions and exemptions, making tax filing simpler.

Up to ₹2,50,000 – Nil

₹2,50,001 to ₹5,00,000 – 5%

₹5,00,001 to ₹10,00,000 – 20%

Above ₹10,00,000 – 30%

Up to ₹4,00,000 – Nil

₹4,00,001 to ₹8,00,000 – 5%

₹8,00,001 to ₹12,00,000 – 10%

₹12,00,001 to ₹16,00,000 – 15%

₹16,00,001 to ₹20,00,000 – 20%

₹20,00,001 to ₹24,00,000 – 25%

Above ₹24,00,000 – 30%

The Budget 2025 has also enhanced the tax rebate under Section 87A to INR 60,000 for incomes up to INR 12,00,000, effectively making income up to INR 12 lakhs completely tax-free under the New Regime for resident individuals. This is a landmark change that dramatically shifts the math for many startup founders.

Despite lower rates in the New Regime, the Old Regime can still be beneficial if taxpayers claim substantial deductions.

Startup founders investing in ELSS, PPF, or LIC policies can claim deductions up to ₹1.5 lakh.

Home loan interest payments up to ₹2 lakh annually can be claimed under Section 24.

Taxpayers can claim deductions for health insurance premiums for themselves, family members, and parents.

Consider Priya, a 34-year-old SaaS startup co-founder earning ₹20 lakh annually.

After applying deductions like HRA, Section 80C, and health insurance premiums, her taxable income reduces significantly.

Without deductions, the taxable income remains higher even though slab rates are lower.

If your startup or MSME files income under Section 44AD (presumptive business income), opting for the New Regime means you lose the benefit of carrying forward business losses. The Old Regime, however, allows you to set off business losses against other income heads, providing significant tax relief in years when your startup runs at a loss – which is common in the first three to five years of operations.

Many startup founders in Tier 1 cities like Mumbai, Bengaluru, and Hyderabad overlook this nuance and switch to the New Regime, only to realise later they have forfeited lakhs in loss set-offs.

There is no single correct answer between the two regimes. The New Regime benefits founders with lower deductions, while the Old Regime may provide greater savings for those with significant investments and expenses.