In today’s competitive and highly regulated business environment, profitability alone is no longer sufficient. Companies must demonstrate efficiency, transparency, and compliance to maintain credibility and stakeholder trust.

A statutory cost audit, mandated under Section 148 of the Companies Act, 2013, plays a crucial role in ensuring this. It requires a detailed and independent review of a company’s cost accounting records for specified industries to ensure accuracy, cost control, and operational efficiency.

This guide provides a clear explanation of the applicability of cost records and cost audit under the Companies (Cost Records and Audit) Rules, 2014, including the industry classifications in Table A (Regulated Sector) and Table B (Non-Regulated Sector).

A cost audit is the verification of a company’s cost accounts and records to ensure that cost accounting principles have been correctly applied. Unlike a financial audit, which focuses on financial statements, a cost audit provides deeper insights into Cost structure, operational efficiency, Resource utilisation, and Cost competitiveness.

The audit is conducted by a qualified Cost Accountant appointed by the Board of Directors, and the final report is submitted to both the company and the Central Government.

Cost Records Maintenance (CRA-1) is required if the company operates in a specified industry (Table A or B) and has a turnover of ₹35 crore or more in the preceding financial year.

Cost Audit (CRA-2/CRA-3/CRA-4) becomes applicable only when additional turnover thresholds are met.

Cost records must be maintained by all companies, including foreign companies, engaged in the production of goods or provision of services listed in the Rules (Table A or B), provided their total turnover is ≥ ₹35 crore in the preceding financial year.

Telecom, electricity, petroleum products, drugs and pharmaceuticals, fertilisers, sugar and industrial alcohol.

A wide list including defence-related machinery, arms and explosives, ports and airport services, iron and steel, cement, construction, textiles, plastics, medical devices, healthcare, education services, and others, with each linked to relevant Customs Tariff headings

Once cost records are applicable under Rule 3, the cost audit becomes applicable only if the company meets both the overall turnover and sector-specific turnover thresholds:

– Overall turnover (all products/services) in the preceding financial year: ₹50 crore or more, and

– Aggregate turnover of the covered product(s)/service(s): ₹25 crore or more.

– Overall turnover (all products/services) in the preceding financial year: ₹100 crore or more, and

– Aggregate turnover of the covered product(s)/service(s): ₹35 crore or more.

Even if a company meets turnover and industry criteria, a cost audit is not applicable if:

These exemptions do not remove the obligation to maintain cost records where applicable; they only waive the cost audit requirement.

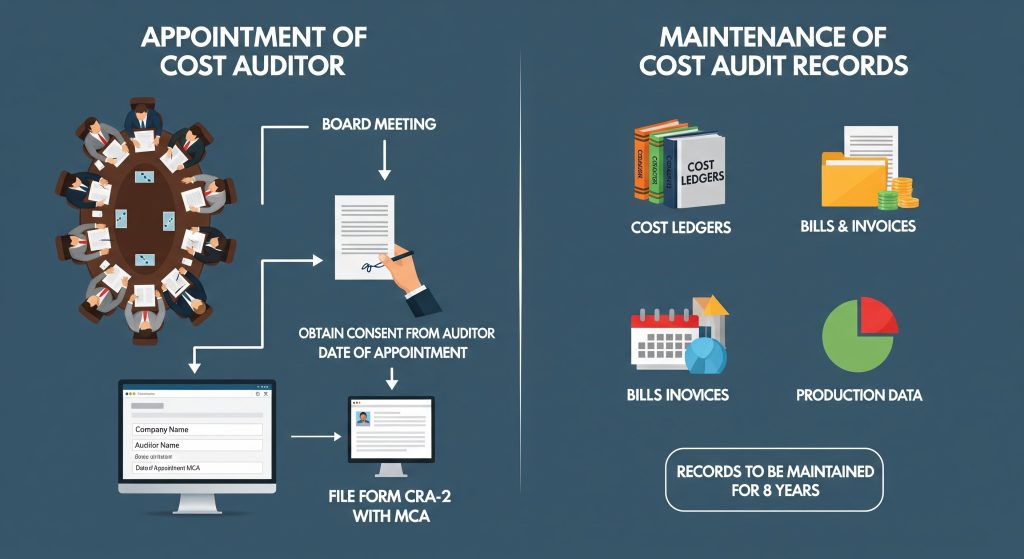

Every company to which the Rules apply must maintain cost records for each financial year starting on or after 1 April 2014 in the manner specified in Form CRA‑1.

Companies that are required to undergo an audit must appoint a Cost Auditor within 180 days of the start of the financial year.

The cost auditor must issue a certificate confirming:

The company must file a notice of appointment with the Central Government within 30 days of Board approval or within 180 days of the start of the financial year (whichever is earlier).

The Cost Auditor must submit the CRA-3 report to the Board within 180 days of the FY closure.

The Board must:

If a company fails to comply with Section 148 or the related Rules, penalties follow the framework of Section 147:

Punishable as per Section 147(1), which generally includes a fine on the company (between ₹25,000 and ₹5,00,000) and on each officer in default (imprisonment up to one year, or fine between ₹10,000 and ₹1,00,000, or both).

Punishable as per Sections 147(2) to 147(4), which include a fine not less than ₹25,000 and up to ₹5,00,000 or four times the auditor’s remuneration, whichever is less, and in willful or fraudulent cases, higher fines and possible imprisonment up to one year, with potential liability to refund remuneration and pay damages.

Effective cost audit practices are essential for ensuring transparency, accuracy, and accountability in financial management. The appointment of a qualified Cost Auditor, along with proper maintenance of cost audit records, enables companies to comply with statutory requirements and improve internal efficiency.