Many businesses across India use the Bill To – Ship To model for drop shipments, third-party deliveries, and supply chain optimization. While this structure has been widely accepted under GST, upcoming changes to the E-Way Bill framework are expected to make compliance more stringent from June 2026.

Businesses involved in indirect deliveries should understand these changes early to avoid future compliance issues, E-Way Bill rejections, and GST notices.

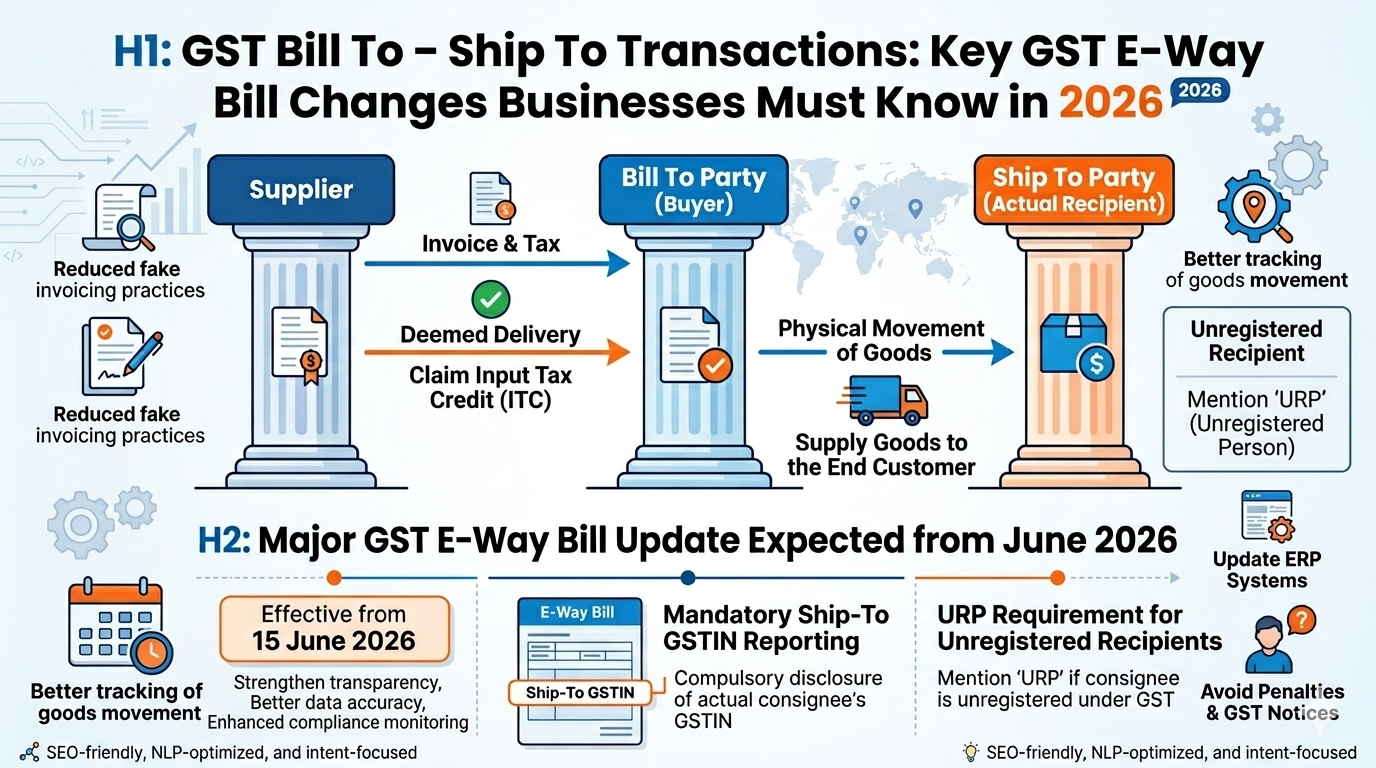

A Bill To – Ship To transaction involves three different parties in a single supply chain arrangement:

In this model, the supplier issues the tax invoice to the buyer, but the goods are delivered directly to another location or customer as instructed by the buyer.

Example

Consider the following scenario:

Although the Delhi company never physically receives the goods, it remains the buyer for GST purposes.

This arrangement is governed by Section 10(1)(b) of the IGST Act, which determines the place of supply in such transactions.

Under GST law, the Bill To party is deemed to have received the goods even when physical delivery takes place at another location.

As a result, the Bill To party can:

Claim Input Tax Credit (ITC)

The buyer remains eligible to claim Input Tax Credit on the buy subject to fulfillment of GST conditions.

Supply Goods to the End Customer

The buyer can legally account for the onward supply of goods to the final customer without any GST complications.

This provision facilitates seamless trade and supports modern supply chain models.

The GST Network is expected to introduce an important compliance need for Bill To – Ship To transactions from 15 June 2026.

Under the proposed update:

Mandatory Ship-To GSTIN Reporting

Businesses generating E-Way Bills may be required to compulsorily mention the Ship-To GSTIN of the actual consignee.

URP Need for Unregistered Recipients

Where the consignee is not registered under GST, taxpayers will need to mention “URP” (Unregistered Person) in the Ship-To GSTIN field.

The goal behind this proposed change is to strengthen transparency in the movement of goods across India.

The proposed amendment is intended to improve GST compliance and strengthen supply chain monitoring.

Key objectives include:

These measures are expected to help authorities identify mismatches and reduce tax evasion risks.

The proposed E-Way Bill change will particularly impact businesses operating through indirect delivery models.

Drop Shipment Businesses

E-commerce sellers, wholesalers, and distributors using drop-shipping arrangements may need to revise their documentation process.

Branch Transfers

Organizations moving goods directly between branches or warehouses should ensure accurate consignee details are captured.

Third-Party Delivery Models

Businesses delivering products directly to end customers on behalf of another entity will need to confirm Ship-To GSTIN information carefully.

To ensure smooth compliance, businesses should begin reviewing their systems and processes well in advance.

Update ERP Systems

ERP software should be configured to capture and confirm Ship-To GSTIN details during invoice generation and E-Way Bill creation.

Review E-Way Bill Procedures

Internal teams responsible for logistics and compliance should understand the revised requirements.

Strengthen Invoice Documentation

Businesses should ensure consistency between:

Accurate documentation can help avoid future disputes and notices.

Failure to follow the updated E-Way Bill requirements may result in:

Early preparation can help businesses avoid operational disruptions once the changes become effective.

The proposed GST E-Way Bill update for Bill To – Ship To transactions represents a significant compliance development for businesses engaged in drop shipping, third-party deliveries, and indirect supply chains.

By ensuring accurate Ship-To GSTIN reporting and aligning ERP systems, invoices, and E-Way Bills, businesses can stay compliant and avoid future challenges.

Organizations that proactively adapt to these changes will be better positioned to maintain smooth logistics operations while meeting evolving GST compliance requirements.