One of the most common questions asked by founders, directors, finance heads, auditors, and compliance professionals is the following:

“Does this Companies Act provision apply to our company?”

In most situations, the answer depends entirely on the company’s financial and structural thresholds.

The Companies Act, 2013, is designed around compliance triggers. Certain legal obligations become mandatory only when a company crosses prescribed limits related to:

Once a threshold is crossed, the compliance requirement becomes automatic. Failure to comply can lead to penalties, director liability, regulatory notices, and governance risks.

For startups, private limited companies, listed entities, LLP advisors, CFOs, company secretaries, and chartered accountants, understanding these thresholds is essential for avoiding non-compliance.

The Companies Act classifies compliance triggers into multiple categories. Understanding these categories helps businesses proactively plan for compliance rather than react after receiving notices.

Financial Thresholds

Based on:

Shareholding-Based Thresholds

Triggered by:

Employee-Related Thresholds

Linked to:

Time-Based Triggers

Connected to:

Structural Thresholds

Applicable based on:

Certain companies must get their annual return certified by a practising company secretary in Form MGT-8.

Threshold

Compliance Requirement

The annual return filed in Form MGT-7 must be certified by a PCS.

Why It Matters

This certification confirms whether the company has complied with major provisions under the Companies Act.

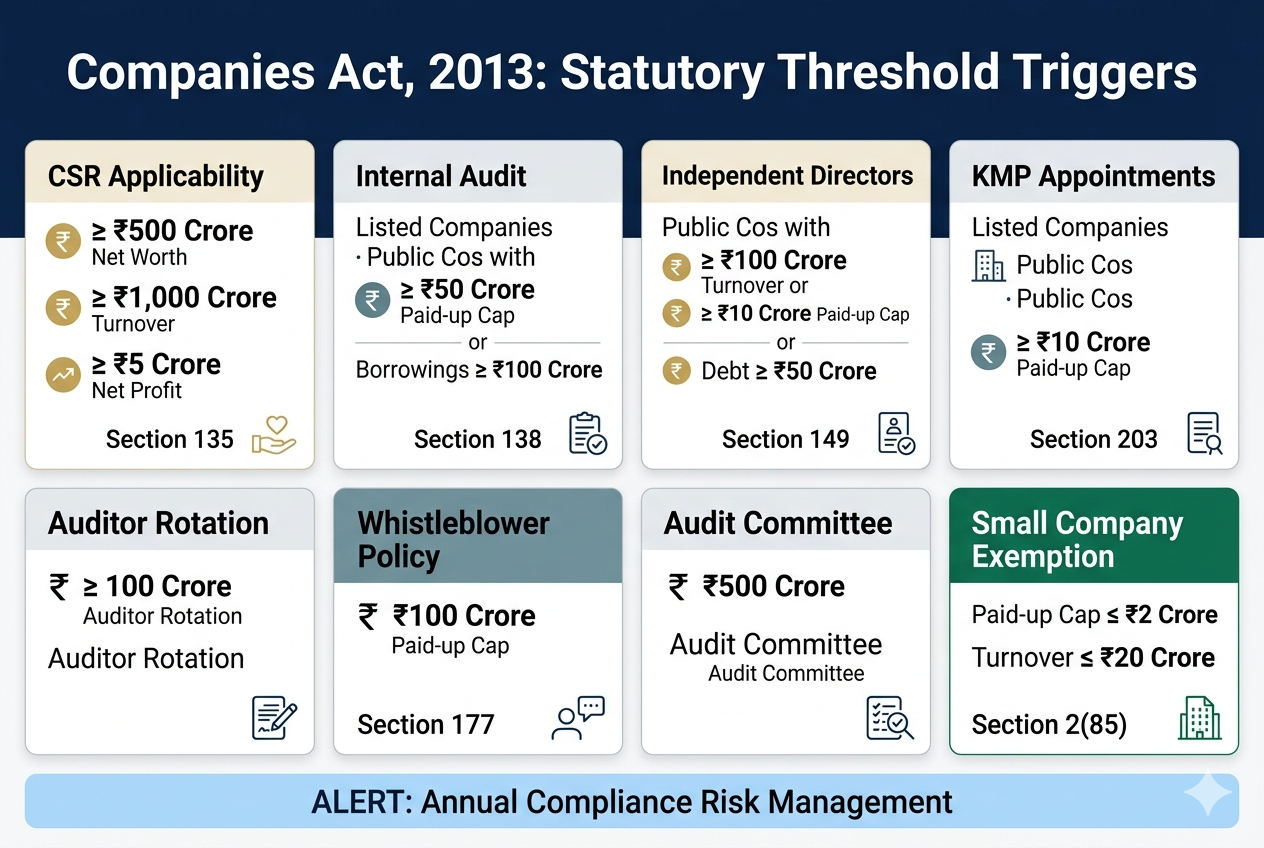

Corporate Social Responsibility (CSR) obligations become mandatory once a company crosses specified financial limits.

Threshold

Any one of the following:

Compliance Triggered

Key Point

CSR applicability is based on financial performance and must be reviewed annually.

The Companies Act requires certain companies to appoint an internal auditor to strengthen internal controls and governance.

Public Company Thresholds

Private Company Thresholds

Listed Companies

Internal audit is mandatory irrespective of size.

Larger companies must follow stricter procedures for the appointment and rotation of statutory auditors.

Public Company Threshold

Private Company Threshold

Compliance Includes

Certain companies are legally required to appoint at least one woman director.

Threshold

Important Rule

Vacancies must be filled within three months.

Independent Directors play a critical role in corporate governance and regulatory oversight.

Threshold

Compliance

At least one-third of the board must consist of independent directors.

Companies required to appoint independent directors must also constitute the following:

Committee Requirements

This committee handles investor complaints and stakeholder grievances.

Threshold

More than 1,000:

Purpose

Ensures investor grievance redressal and governance transparency.

Whistle-Blower Policy / Vigil Mechanism – Section 177

Certain companies must implement a formal vigil mechanism.

Threshold

Compliance

Larger companies must appoint full-time Key Managerial Personnel.

Threshold

Mandatory KMP Positions

Private companies also face mandatory CS appointments once they cross a prescribed capital limit.

Threshold

Paid-up capital ≥ ₹10 crore

Compliance

Appointment of a whole-time Company Secretary.

H2: Secretarial Audit Requirement – Section 204

Certain companies must undergo a Secretarial Audit conducted by a Practising Company Secretary.

Threshold

Output

Secretarial Audit Report in Form MR-3.

Companies crossing certain thresholds must file financial statements in XBRL format.

Threshold

Compliance

Filing of AOC-4 XBRL.

The Companies Act also provides compliance relief to qualifying small companies.

Eligibility

Both conditions must be satisfied:

Benefits

Many startups and MSMEs unknowingly cross threshold limits after:

Once thresholds are crossed, compliance obligations begin automatically. Delayed implementation can result in:

Businesses should conduct an annual threshold review at the beginning of every financial year.

Tracking Companies Act thresholds helps businesses:

For scaling startups and mid-sized companies, threshold monitoring is no longer optional — it is a critical governance requirement.

The Companies Act, 2013 operates heavily through threshold-based compliance triggers. As companies grow in capital, turnover, profitability, and borrowing exposure, additional governance and reporting obligations automatically apply.

From CSR and Internal Audit to Independent Directors, Secretarial Audit, KMP appointments, and XBRL filings, each threshold carries legal and operational implications.

Businesses that proactively monitor these limits can avoid regulatory surprises, maintain stronger governance standards, and build long-term credibility with investors, banks, regulators, and stakeholders.