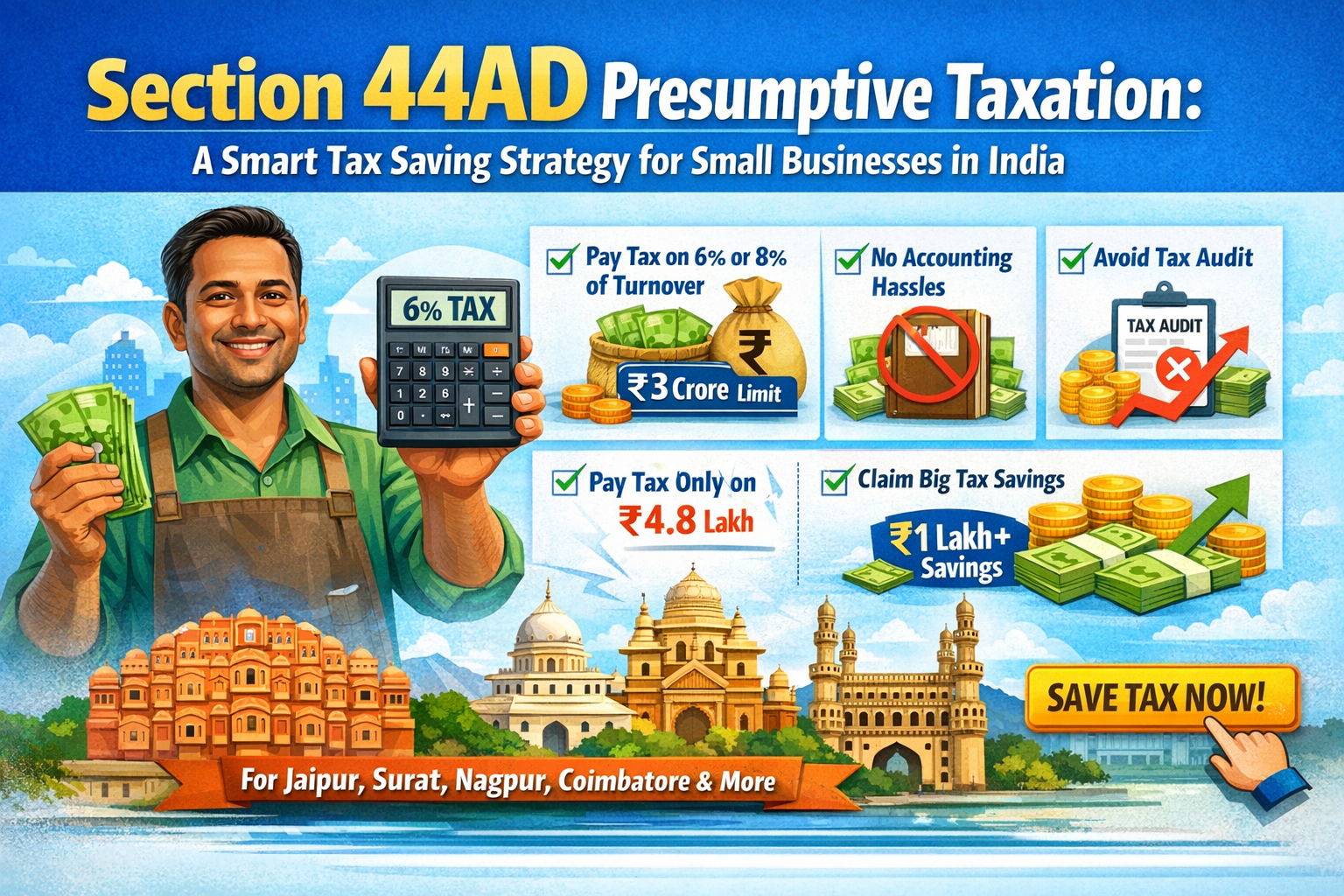

Small business owners in Jaipur, Surat, Nagpur, and Coimbatore struggle with taxes. Tax rules feel complex and take too much time to navigate. Income tax Section 44AD—the Taxation Scheme—makes it simple. It cuts your tax burden and speeds up compliance.

Even though this scheme has clear benefits, many MSMEs do not use it as much as they could. Learning how it works can help you save money, reduce paperwork, and avoid extra audits.

Section 44AD lets eligible businesses report a set percentage of their turnover as income. No need for detailed books or records.

This means you do not need to track every expense or maintain full books of accounts. Your taxable income is calculated on a presumptive basis.

Let’s say your business turnover is ₹80 lakhs in a financial year and most payments are received digitally.

Even if your real profit is much higher, say ₹20 lakhs, you still pay tax only on ₹4.8 lakhs. This makes Section 44AD a truly valuable and effective tax-saving option for small businesses.

This scheme is available to:

Eligibility Conditions:

You cannot use this scheme if you fall under these categories:

One of the biggest advantages of Section 44AD is the lower tax rate for digital transactions.

If your customers pay via UPI, bank transfer, or card:

Example:

This ₹4 lakh difference can save you up to ₹1 lakh in taxes. Encouraging digital payments directly increases your tax savings.

While Section 44AD is beneficial, it comes with an important condition.

If you opt for this scheme and later decide to exit:

Important Tip:

Avoid switching out of the scheme without proper planning, even in low-profit years.

Is your startup a professional service? Think IT consulting, architecture, medical practice, legal advice, or accounting. You qualify for Section 44ADA—not 44AD.

The rules work similarly.

Example: A freelance IT consultant earns ₹40 lakhs yearly. They declare ₹20 lakhs as taxable income. These beats tracking real profits if your actual margins are higher.

Filing under this scheme is simple:

Due Date:

India has over 6 crore MSMEs and micro-enterprises. Section 44AD is a real tax benefit from the Income Tax Act. It reduces accounting work, skips audits, and often legally lowers your tax bill.

Are you a small business owner in Jaipur, Surat, Coimbatore, Nagpur, or Ahmedabad? Is your turnover under ₹3 crores? Talk to a qualified CA now if you haven’t tried this. Missing it could cost you ₹1 lakh or more each year.