Companies are required to report all deposits and certain exempted deposits in e-Form DPT-3 under the Companies (Acceptance of Deposits) Rules, 2014. A common area of confusion is how to report loans taken from shareholders whether they are treated as deposits or exempted deposits. Proper classification is crucial to avoid penalties and compliance issues.

Loans taken from shareholders are not automatically exempt under the Companies Act. The reporting depends on whether the loan fits specific sub-clauses of Rule 2(1)(c). Loans that do not fall under these sub-clauses are treated as deposits and must be reported as such in DPT-3. This applies especially to private companies, where non-director shareholder loans are allowable under exemptions but reported as deposits, not exempt.

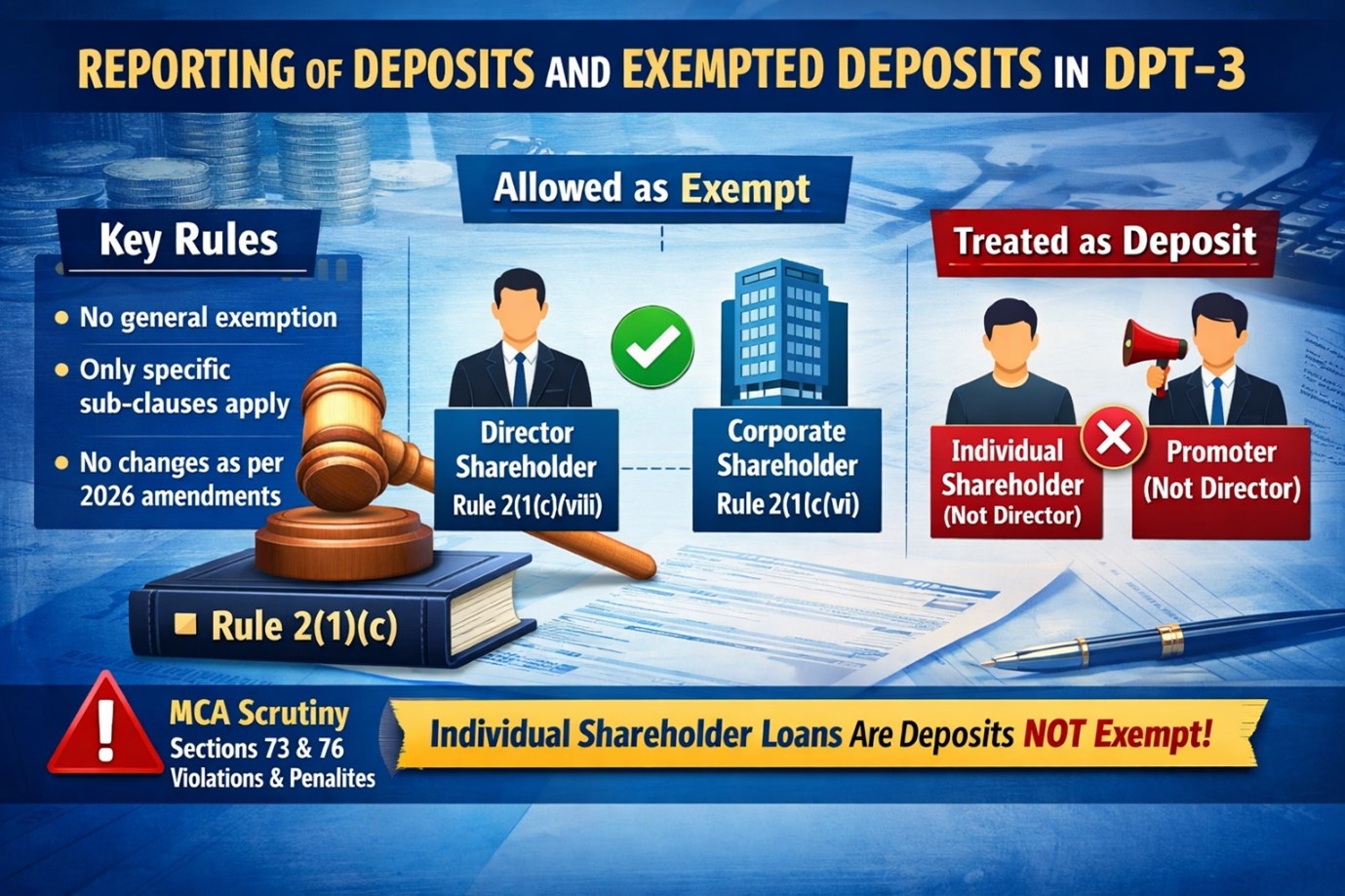

The key provision is Rule 2(1)(c) of the Companies (Acceptance of Deposits) Rules, 2014.

There is no general exemption for loans from shareholders under Rule 2(1)(c).

A shareholder loan is reportable as “not considered as deposit” only if it fits into a specific sub-clause of Rule 2(1)(c). No changes in 2026 amendments alter this core rule.

DPT-3 field to select: “Amount received from a director”

Example:

If Mr. A is a shareholder and also a director, and he lends INR 50 lakh from his personal funds, it can be reported as exempt.

Note: Corrected clause reference to (vi) for amounts from other companies, but (vii) aligns for specifics.

Eligible cases:

DPT-3 field to select: “Loan received from any other company”

Example:

If XYZ Pvt. Ltd., a corporate shareholder, lends INR 1 crore, it can be reported as exempt under this clause.

What you CANNOT select

There is no separate field or clause in DPT-3 for:

Shareholder Status | Clause under 2(1)(c) | DPT-3 Reporting |

Director + shareholder | 2(1)(c)(viii) | Allowed as exempt |

Corporate shareholder | 2(1)(c)(vii) | Allowed as exempt |

Individual shareholder (non-director) | None | Treated as deposit |

Promoter but not director | None | Treated as deposit |

Incorrectly classifying shareholder loans as exempt in DPT-3 is a common point of MCA scrutiny. This can trigger:

Best practice: Always check if the shareholder is a director or corporate entity before claiming exemption. For private companies, confirm exemption applicability.

Loans from shareholders in DPT-3 must be carefully classified to ensure compliance. Only loans from directors or corporate shareholders can be treated as exempt deposits under Rule 2(1)(c). All other loans, including those from individual shareholders or promoters who are not directors, are considered deposits and must be reported accordingly in private companies. Accurate reporting helps the company avoid penalties and MCA scrutiny under Sections 73 and 76.

Compliance Related to Unspent CSR Amount: Deposit, Transfer, or Spend? The Real Rules

Compliance Related to Unspent CSR Amount: Deposit, Transfer, or Spend? The Real Rules GSTR-3B New Rules from Jan 2026: Full GST Guide

GSTR-3B New Rules from Jan 2026: Full GST Guide Undisclosed Foreign Assets: What Taxpayers Need to Know under Budget 2026–27

Undisclosed Foreign Assets: What Taxpayers Need to Know under Budget 2026–27 Large Value Funds (LVFs): SEBI’s 2025 Reforms and Their Impact on Institutional Capital

Large Value Funds (LVFs): SEBI’s 2025 Reforms and Their Impact on Institutional Capital Key Clauses of a Partnership Deed in IndiaCompliance Related to Unspent CSR Amount: Deposit, Transfer, or Spend? The Real RulesGSTR-3B New Rules from Jan 2026: Full GST GuideUndisclosed Foreign Assets: What Taxpayers Need to Know under Budget 2026–27Large Value Funds (LVFs): SEBI’s 2025 Reforms and Their Impact on Institutional CapitalKey Clauses of a Partnership Deed in India

Key Clauses of a Partnership Deed in IndiaCompliance Related to Unspent CSR Amount: Deposit, Transfer, or Spend? The Real RulesGSTR-3B New Rules from Jan 2026: Full GST GuideUndisclosed Foreign Assets: What Taxpayers Need to Know under Budget 2026–27Large Value Funds (LVFs): SEBI’s 2025 Reforms and Their Impact on Institutional CapitalKey Clauses of a Partnership Deed in India