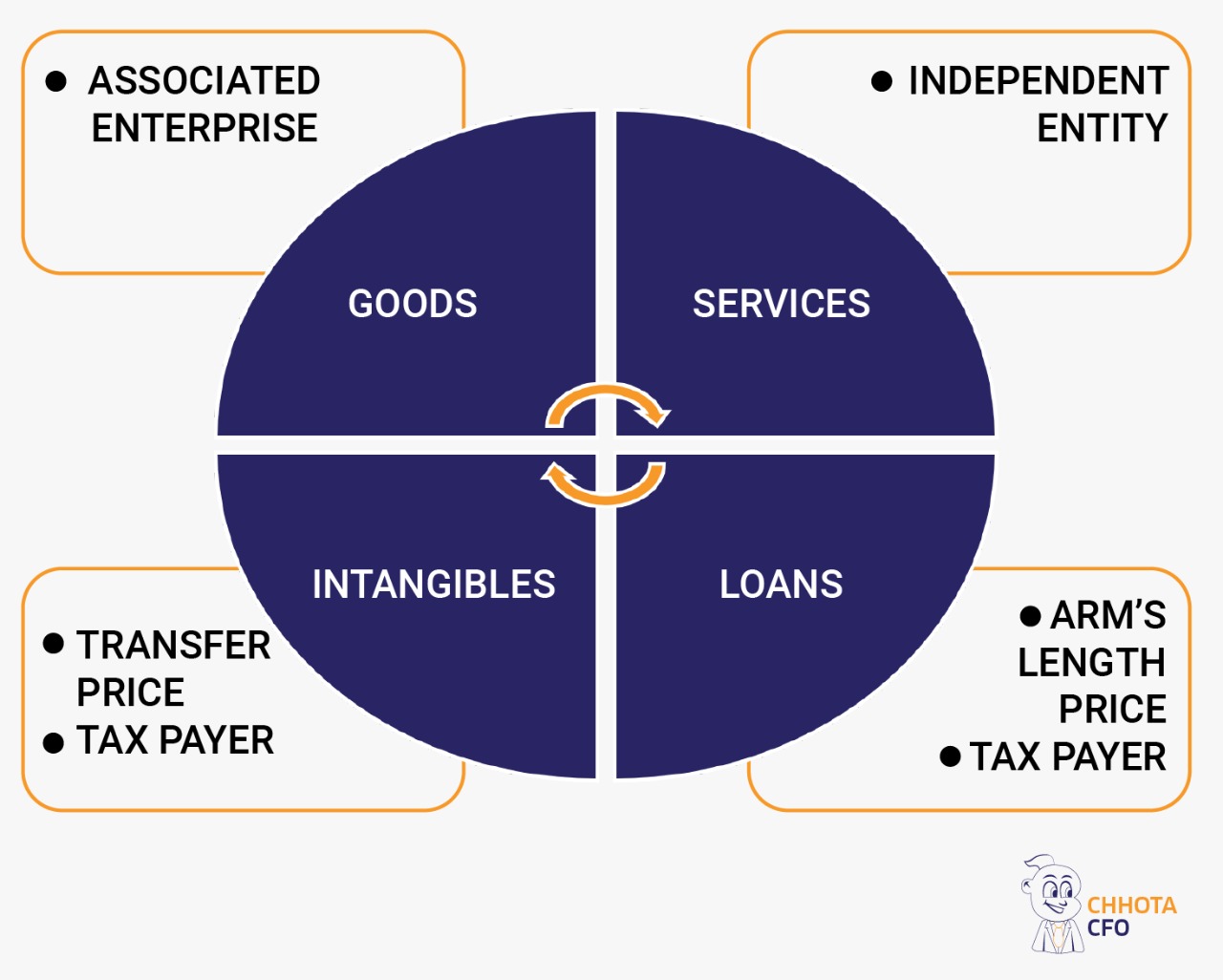

ITP refers to the prices at which a company undertakes cross border transactions with associated enterprises. These transactions can include tangible goods, in tangible property, services and financing transactions.

Every person who has entered into an international transaction and aggregate value of such transactions exceeds Rs. 1 crore during the financial year. In case the aggregate value of such transactions does not exceed Rs. 1 crore, it is not mandatory to maintain the information and documents.

Lowering duty costs by shipping goods into high tariff countries at minimal and transfer prices so that duty base and duty are low. Reducing income taxes in high tax countries by over pricing goods transferred units in such countries profits are eliminated and shifted to low tax countries.

Business enterprises often are organised by division. A division may be a profit centre responsible for revenues and operating expenses or investment centre responsible for also assets.

Allowing local managers to respond quickly to a changing environment

Dividing large, complex problems into manageable prices.

Motivating local managers who otherwise will be frustrated if asked only to implement the decisions of others.

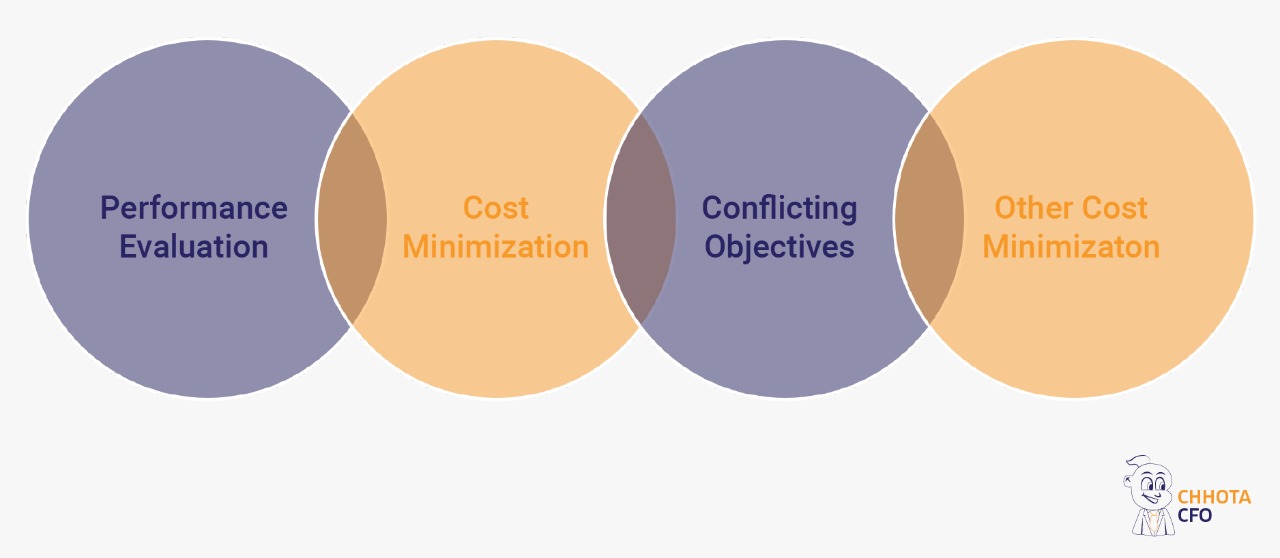

Two factors heavily influence the manner in which ITP are determined.

The first factor is the objective that headquarters management wishes to achieve through its transfer pricing practises. One possible objective relates to management control and performance evaluation. Another objective relates to the minimization of one or more types of costs. The second factor affecting international transfer pricing is the law that exists in most countries governing the manner in which intercompany transaction crossing their borders may be priced. These laws were established to make sure the multinational companies are not able to avoid paying their fair share of taxes import duties.

SCHEMES OF TRANSFER PRICING PROVISIONS IN INDIA

Relevant provisions under section 92

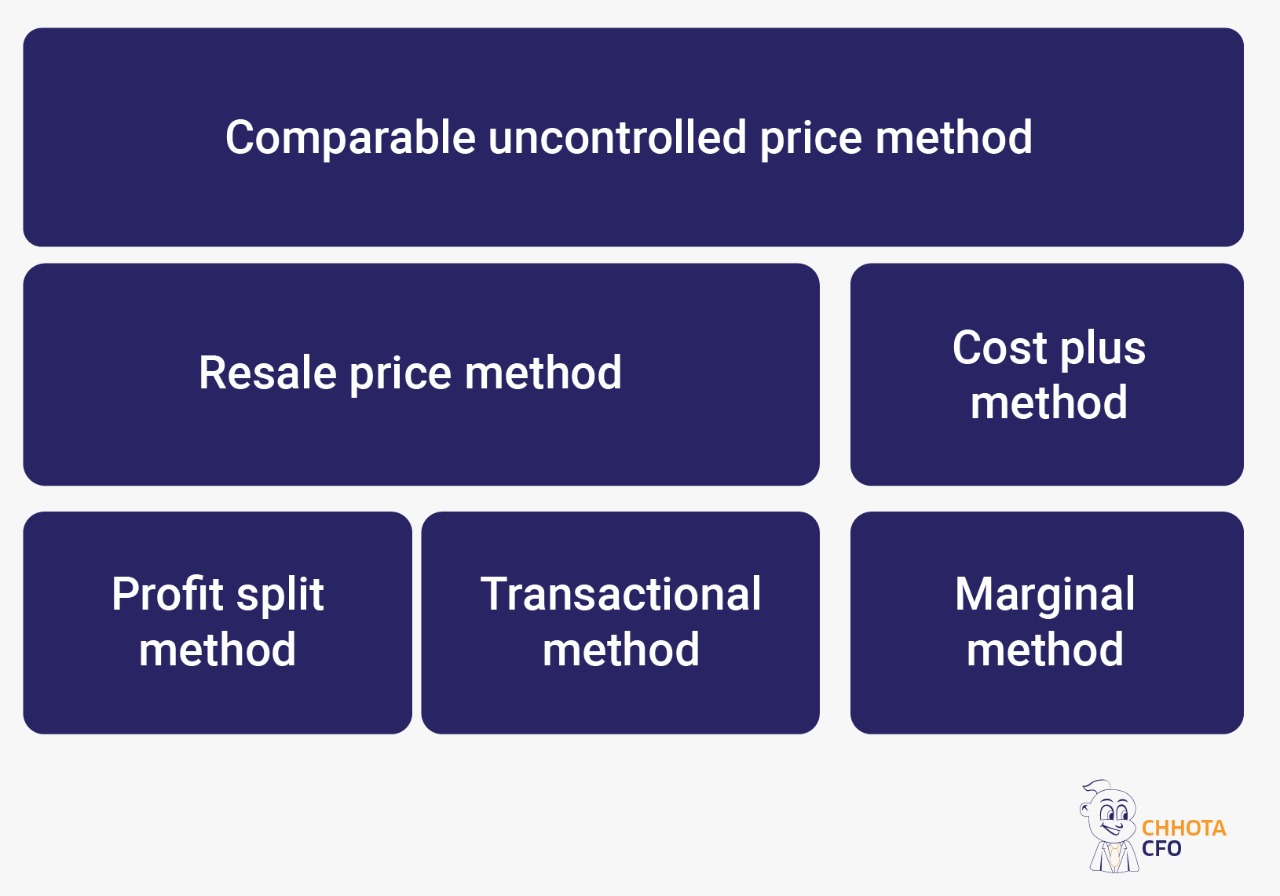

Computation of income from IT having regard to Arm’s length price